Disability Income Insurance: How Today’s Decisions Impact Tomorrow’s Choices

By Michael Sullivan | Posted July 27, 2015

Disability Income Insurance: How Today’s Decisions Impact Tomorrow’s Choices

Doctors and dentists nationwide clearly understand the importance of having disability income insurance (DI) to protect the time and money they’ve invested in their profession. And most have considered at length what would happen to them, their incomes, their families and their careers if they suddenly found themselves injured or ill – leading them to seek the protection a DI policy provides.

So what’s the problem? DI is a complex buying decision – with varying stipulations in policy contracts that impact the type of benefits a policy owner might receive at time of claim. The problem is that busy medical and dental professionals can’t find the time to fully understand key concepts in their policies, and many would be surprised to find how those details could affect them at the time of claim.

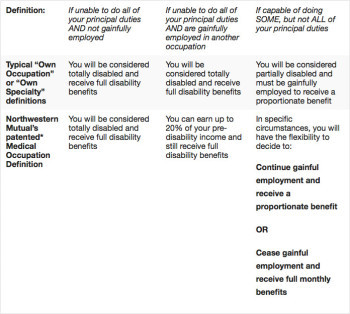

Many doctors think that if they are unable to perform their principal medical duty, their “bread and butter,” they would be totally disabled and receive full disability benefits. But that’s not typically the case with “own occupation” coverage (the kind of DI that has traditionally been recommended for medical and dental professionals). It would only be true if the insurance company determines that they have only one principal duty at the time of claim. And, of course, most medical professionals have more than one principal duty.

Consider the example of a surgeon, whose primary source of income comes from performing surgery, but who also does non-surgical patient consultations. If this surgeon suffers a hand injury and is no longer able to perform surgery, they would likely consider themselves totally disabled. However – based on typical “own occupation” and even “own specialty” definitions – if they are still able to consult with patients, they may be considered partially disabled and would receive only partial disability benefits.

To help eliminate this kind of misperception, Northwestern Mutual introduced the patented* “Medical Occupation Definition” of total disability. The only definition of its kind in the industry, it was designed specifically for – and with input from – the physicians and dentists it impacts.

The Medical Occupation Definition differs from typical “own occupation” and “own specialty” definitions because it provides physicians, dentists and podiatrists, in certain situations, the flexibility to choose between continuing to work and receiving a partial benefit, or not working at all and receiving full benefits. This is an important difference that typical “own occupation” and “own specialty” definitions do not offer at the time of claim.

Consider the chart at right, which outlines how the definitions compare in various circumstances:

Unfortunately, no one can predict the type of disability they will have, or control whether that disability will prevent them from doing their job (or seeking alternative employment). This is why the flexibility of the Medical Occupation Definition is so critical; at a time when so much hangs in balance, it provides medical professionals a choice about their future.

Northwestern Mutual has created an online tool called the “Disability Income Insurance Knowledge Center for Physicians and Dentists” that illustrates how the Medical Occupation Definition compares with other definitions of total disability. Medical professionals are invited to visit Todd G Grantham’s website at toddgrantham.com to access the tool, enter information about their practice, and find out for themselves how each definition would impact them at the time of claim.

The definition used in your policy is just one of the variables that must be considered carefully when choosing disability insurance. Although the prospect of having to rely on any type of disability insurance is something no one likes to think about, taking the time to do so can lead to a vitally important outcome: knowledge that what you want and what you need matches what your policy can do for you.

*U.S. Patent No. 8,775,216, issued on methods and systems for processing insurance claims in accordance with disability income insurance policies the scope of which cover the Medical Occupation Definition of disability.